What is the Zero Trust Security Market Overview – definition, scope, and significance?

Zero Trust Security is a strategic approach that assumes no user, device, or network traffic is trustworthy by default, requiring continuous verification before granting access to resources. The market encompasses solutions and services that implement identity‑centric authentication, micro‑segmentation, secure connectivity, and threat detection across on‑premise and cloud environments. Its significance lies in addressing sophisticated cyber‑threats, compliance pressures, and the shift to hybrid work models, making Zero Trust a cornerstone of modern enterprise security architectures.

What are the main drivers, restraints, challenges, and opportunities in the Zero Trust Security Market?

Key drivers include rising ransomware incidents, regulatory mandates for data protection, and the rapid adoption of cloud services that expose traditional perimeter defenses. Restraints involve high implementation costs and complexity of integrating legacy systems. Challenges center on talent shortages and the need for seamless user experience during continuous verification. Opportunities arise from emerging technologies such as AI‑enhanced analytics, the growing demand for secure remote access, and the expansion of Zero Trust as a service (ZTaaS) models.

What current and emerging growth trends are shaping the Zero Trust Security Market?

The market is trending toward unified platforms that combine identity governance, network security, and endpoint protection under a single policy engine. Emerging trends include the integration of Zero Trust principles with Secure Access Service Edge (SASE), increased use of multi‑factor authentication (MFA) powered by biometric factors, and the deployment of Zero Trust across IoT and industrial control systems. Vendors are also focusing on automating policy enforcement through orchestration and intent‑based networking.

How has COVID‑19 impacted the Zero Trust Security Market and what is the recovery trajectory?

The pandemic accelerated remote work, exposing gaps in traditional perimeter‑based security and driving rapid adoption of Zero Trust solutions. Organizations rushed to secure cloud applications and VPN alternatives, boosting market demand. Post‑pandemic, the momentum continues as hybrid work becomes permanent, sustaining robust growth. The recovery trajectory is positive, with enterprises allocating larger portions of IT budgets to Zero Trust initiatives to mitigate lingering security vulnerabilities.

Who are the major competitors in the Zero Trust Security Market and what is the state of market consolidation?

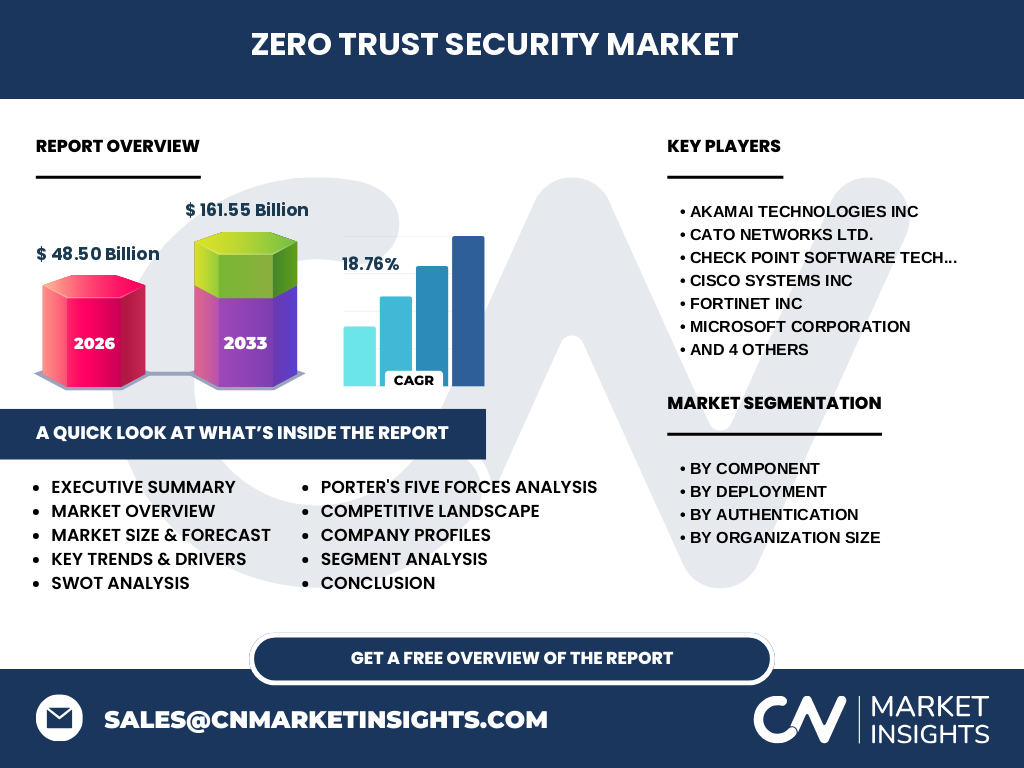

Leading competitors include Akamai Technologies, Cato Networks, Check Point Software Technologies, Cisco Systems, Fortinet, Microsoft, Okta, Palo Alto Networks, VMware, and Zscaler. The market is moderately consolidated, with a few large vendors offering end‑to‑end portfolios while niche players focus on specialized components such as identity verification or cloud‑native firewalls. Recent strategic acquisitions and partnerships indicate ongoing consolidation aimed at broadening solution breadth and enhancing integration capabilities.

What are the key findings in the Executive Summary of the Zero Trust Security Market?

The Zero Trust Security Market is projected to reach $48.50 billion in 2026 and $161.55 billion by 2033, reflecting a robust CAGR of 18.76 %. Growth is propelled by heightened cyber‑risk awareness, cloud migration, and regulatory pressures. Solution and service components dominate, with demand for cloud deployment and multi‑factor authentication rising across both SMEs and large enterprises. Competitive dynamics show strong innovation pipelines and strategic collaborations among top vendors.

What are the forecasted market expectations for 2025‑2032?

Based on the given CAGR of 18.76 %, the market will continue its accelerated expansion, maintaining double‑digit growth each year. Enterprises are expected to increase investment in Zero Trust architectures, favoring cloud‑native deployments and integrated service models. The forecast underscores a sustained shift from perimeter security to identity‑centric controls, with emerging markets adopting Zero Trust faster as digital transformation initiatives mature.

How is the Zero Trust Security Market sized and shared by segmentation?

Segmentation by component reveals a split between solutions (software, platforms) and services (consulting, integration). Deployment segmentation shows on‑premise versus cloud, with cloud gaining a larger share due to scalability and remote‑work demands. Authentication segmentation highlights single‑factor versus multi‑factor authentication, where MFA is experiencing faster adoption. Organization size segmentation indicates both SMEs and large enterprises are investing, though large enterprises lead in comprehensive Zero Trust rollouts.

What is the global Zero Trust Security Market size and share by region?

While specific regional monetary values are not disclosed, the market’s global footprint encompasses North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa. Each region contributes to the overall $48.50 billion valuation in 2026, with growth driven by regional digital transformation agendas, regulatory frameworks, and the prevalence of high‑value target industries.

What are the detailed regional performances in the Zero Trust Security Market?

North America leads due to early adoption of advanced security frameworks and strong vendor presence. Europe follows, propelled by GDPR compliance and robust cloud adoption. Asia‑Pacific exhibits the highest growth potential, driven by rapid enterprise digitization and increasing cyber‑threats. Latin America and the Middle East & Africa are emerging markets, showing incremental uptake as organizations modernize legacy infrastructures.

Which companies lead the Zero Trust Security Market and what are their strategic approaches?

Top players such as Cisco, Microsoft, Palo Alto Networks, and Zscaler focus on integrated platforms that combine networking, identity, and threat intelligence. Fortinet emphasizes high‑performance hardware‑accelerated firewalls with Zero Trust policies. Okta specializes in identity and access management, expanding its MFA suite. Akamai leverages its edge network for secure access, while Cato Networks promotes SASE‑aligned Zero Trust solutions. These firms invest heavily in R&D, strategic alliances, and acquisitions to broaden their ecosystems.

How does Porter’s Five Forces assessment apply to the Zero Trust Security Market?

Threat of new entrants is moderate due to high entry barriers like technology expertise and brand trust. Bargaining power of buyers is increasing as enterprises demand flexible, subscription‑based models. Supplier power is low because core components (software, cloud infrastructure) are commoditized. Threat of substitutes is limited; traditional perimeter defenses cannot replace Zero Trust capabilities. Competitive rivalry is intense, driven by rapid innovation and overlapping solution portfolios.

What are the SWOT findings for the Zero Trust Security Market?

Strengths: Strong demand, alignment with regulatory trends, and clear ROI in breach reduction. Weaknesses: Implementation complexity and skill gaps. Opportunities: Expansion into emerging economies, integration with AI/ML, and growing Zero Trust as a service market. Threats: Possible market saturation and evolving threat vectors that may outpace current Zero Trust controls.

What does the value chain of the Zero Trust Security Market look like?

The value chain starts with research & development of authentication algorithms and micro‑segmentation techniques, followed by product engineering and platform integration. Vendors then deliver solutions through direct sales, channel partners, or cloud marketplaces. Implementation services, managed security services, and ongoing support constitute downstream activities, creating recurring revenue streams and fostering customer lock‑in.

What key investment insights can be drawn for the Zero Trust Security Market?

Investors should target companies with strong cloud‑native portfolios, diversified revenue from both solutions and services, and demonstrable integration capabilities with SASE and IAM ecosystems. Companies that pursue strategic acquisitions to fill functional gaps or expand geographic reach are positioned for accelerated growth. Monitoring partnership announcements with hyperscale cloud providers can also indicate future market leadership.

What are the main conclusions of the Zero Trust Security Market analysis?

The Zero Trust Security Market is on a steep growth trajectory, underpinned by the need for resilient, identity‑centric security in a distributed work environment. With a projected CAGR of 18.76 % and a market size reaching $161.55 billion by 2033, the sector offers substantial opportunity for vendors, investors, and enterprises seeking to modernize their security postures. Continuous innovation and seamless integration will differentiate market leaders.

How was the research methodology for this report conducted?

The research combined primary interviews with industry executives, secondary data from vendor financials, market surveys, and reputable publications. Quantitative data were validated through triangulation across multiple sources, while qualitative insights were derived from expert opinion panels. Forecast modeling applied the stated CAGR to project future market size, ensuring alignment with known macro‑economic and technology adoption trends.

What is the scope of this research and its limitations?

The scope covers global Zero Trust Security market dimensions, segmentation by component, deployment, authentication, and organization size, as well as regional analysis and competitive profiling of the ten listed key companies. Limitations include the exclusion of proprietary financial details beyond the supplied figures and the omission of granular market share percentages for individual regions or vendors.

Which key companies have recent developments in the Zero Trust Security Market?

Recent announcements include Cisco’s launch of an AI‑driven Zero Trust analytics platform, Microsoft’s integration of Zero Trust policies into Azure Active Directory, and Palo Alto Networks’ acquisition of a SaaS‑based MFA provider. Zscaler expanded its cloud security stack with a new data‑loss‑prevention module, while Okta introduced passwordless authentication leveraging WebAuthn. Fortinet unveiled a next‑generation firewall optimized for Zero Trust micro‑segmentation, and Cato Networks announced a partnership with a leading telecom to deliver Zero Trust SASE at the network edge.